In the tech ecosystem, generative AI (GenAI) has become a game changer in customer service and support. A Bloomberg Intelligence report estimates that the GenAI market will hit $1.3 trillion by 2032, up from $40 billion in 2022. However, while many companies remain bullish about deploying AI customer support, most still underestimate the requirements for deployment, according to an MIT Technology Review Insights global study.

How to Implement AI Without Destroying Customer Trust

Successfully deploying Gen-AI without disrupting customer trust and loyalty requires a systemic approach. This article will present a three-step roadmap for organizations while traversing this transformative journey.

Step 1. Build an AI-ready organization

The first step to successfully deploy AI customer support software into your CS is to adopt a data-centered mindset. By this, we mean combining data strategy, setting up the necessary data governance mechanisms and initial infrastructure, and implementing organization-wide data literacy programs.

An effective data strategy will spearhead all the decision-making regarding technology selection and assessment of use cases. Some of the questions leaders must ask include:

What functions could Gen-AI assist with?

How will AI improve our services or operations?

By answering these questions, leaders will be better placed to translate strategy into actionable roadmap.

Step 2. Out with the old in with the new

Once you’ve established a data strategy, the next step is to clean the knowledge base and customer data. Michael Boz, senior VP of innovation strategy at Salesforce, says that when businesses incorporate Gen-AI into poor customer self-service, they are only worsening the situation, albeit on a grander scale and with more severe repercussions than before.

Imagine an AI customer service software that always provides incorrect information due to a flawed underlying knowledge base. It will only become more proficient with Gen-AI. The only difference is that it will now be more confident disseminating false information, not because it is merely hallucinating.

Ed Thompson, senior VP of marketing at Salesforce, sees another route to implementing Gen-AI. According to Ed, old or unreliable knowledge base data is better off being scrapped altogether and the knowledge base filled with new content from scratch.

He further says that more than 40% of businesses begin from scratch knowledge acquisition from customer chats, emails, calls, etc. These businesses experience faster and more accurate creation of knowledge sources and a dramatically reduced risk of delusions.

Step 3. Getting it right for the customer

The secret to effectively adopting Gen-AI customer support bot lies in taking decisive action rather than getting paralyzed in a cycle of overanalyzing. You can start by identifying a specific use case and moving forward decisively.

Then, you can form cross-functional teams and employ a culture of experimentation and learning to reap the full benefits of GenAI. Leaders don’t lie around waiting for a solution – no! They identify a specific opportunity to benefit their customers and build around it.

Conclusion

Successfully deploying Gen-AI without disrupting customer trust requires strategic planning. It involves redefining your legacy systems and optimizing how you collect, analyze, and apply data to make faster, more informed decisions that add value to your customers. The key is to prepare your organization for the rollout, from forming teams to deploying the technology and customer engagement.

FinTech app development cost is critical for all financial companies planning to digitize their business processes. To estimate the detailed price, you should consider a wide variety of aspects, such as functionality, design complexity, platforms to cover, and architecture requirements. However, the most influenceable factors are development time and specialists’ hourly wages.

In this article, we provide a comprehensive coverage of calculating the approximate time and cost to create FinTech applications of diverse types, from banking to investment apps. This ensures that you, as financial professionals, are well-informed and catered to your specific needs.

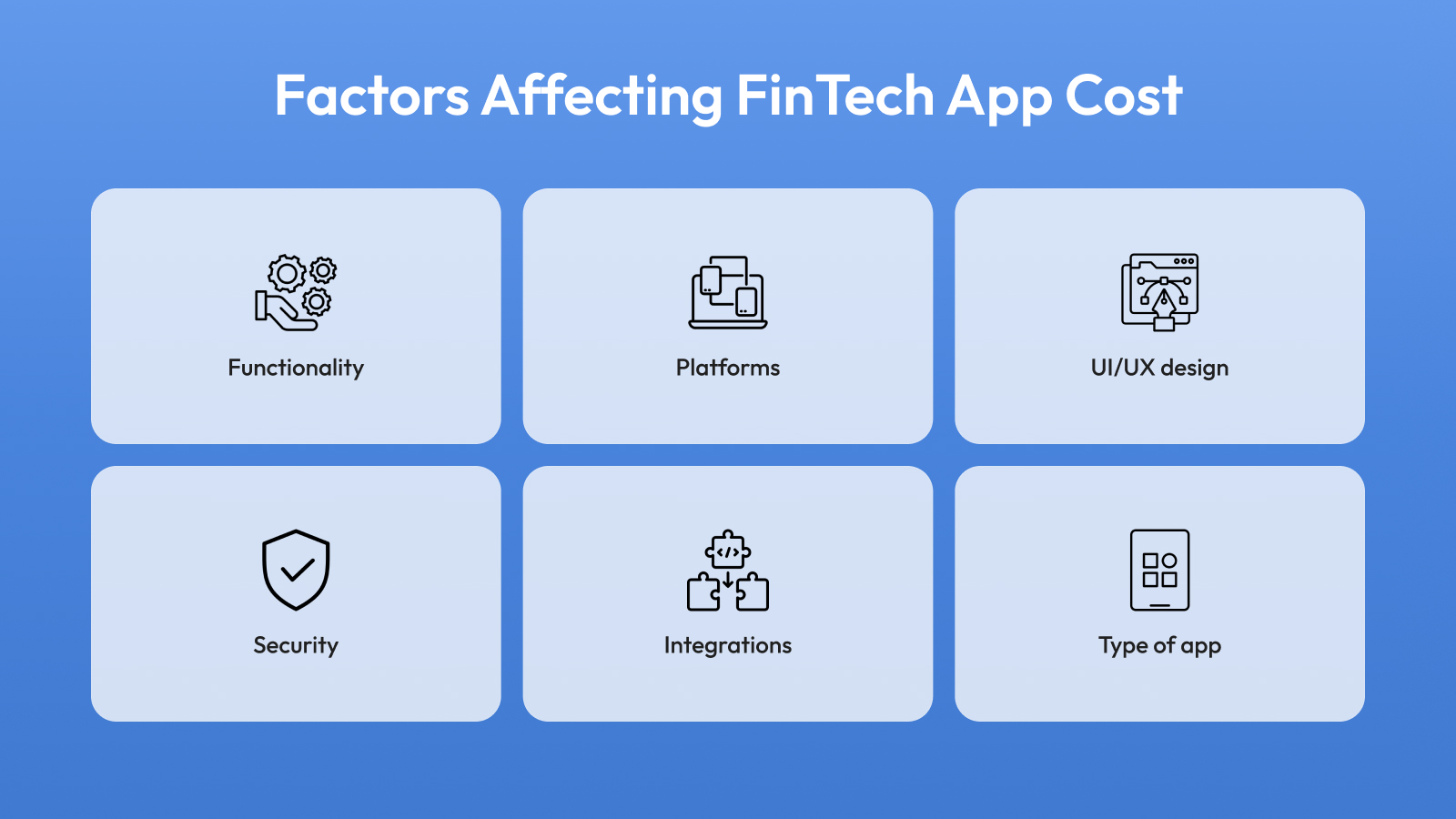

Main Factors Influencing The Cost Of Creating FinTech Application

You might be wondering what aspects are the most critical to consider when estimating FinTech app cost. In this section, we will describe the main factors in detail:

Diversity and complexity of functionality

The functionality of your application significantly impacts the total price. More features require more time to develop, which increases the overall project duration. Moreover, you may need more complex technologies and deeper expertise to implement intricate functions.

Platforms to cover

Crafting an app for one platform (iOS or Android) requires less time, a smaller development team, and shorter resources than creating two separate native applications. However, if you aim to cover both platforms and want to reduce investments, here’s the deal: you can opt for cross-platform Flutter app development. Such a service allows the creation of two applications in a single code base, significantly reducing the cost of making a FinTech app. Flutter is a popular cross-platform framework that has been used to develop some of the best Flutter apps in recent years.

UI/UX design

Your app’s design is key to its success and appeal. You can use one of the popular templates to design your solution at a lower cost, but such a decision may reduce your competitiveness. If you want to engage more users, you should turn to a custom UI/UX design. But here’s the kicker: the cost of FinTech app design will also vary based on complexity: many pages with a variety of interactive elements increase the final price.

Security and compliance

Financial applications require a special approach to data protection since they operate sensitive user data. Moreover, FinTech solutions adhere to strict industry regulations that demand implementing particular functionality to ensure compliance. You can integrate only basic security measures that enable you to comply with regulations to lower initial investments. However, we highly recommend improving your app’s protection with robust tools such as biometric authentication, industry-specific data encryption, etc.

Integrations

Suppose you want to build a FinTech app integrated with other software solutions in your business ecosystem. In that case, you should be ready to spend initial costs to provide seamless interaction. Moreover, expanding your platform’s capabilities with third-party service integrations can also increase the overall project price. This is wild, but these expenses are only for the best: your FinTech app will be able to provide a seamless user experience and attract more clients.

Type of FinTech app

There are various types of financial applications, each of which requires the implementation of unique features and sometimes adheres to distinct regulations and laws. Accordingly, the cost of a FinTech app can change from type to type. For example, banking solutions require more development time than landing or investment apps.

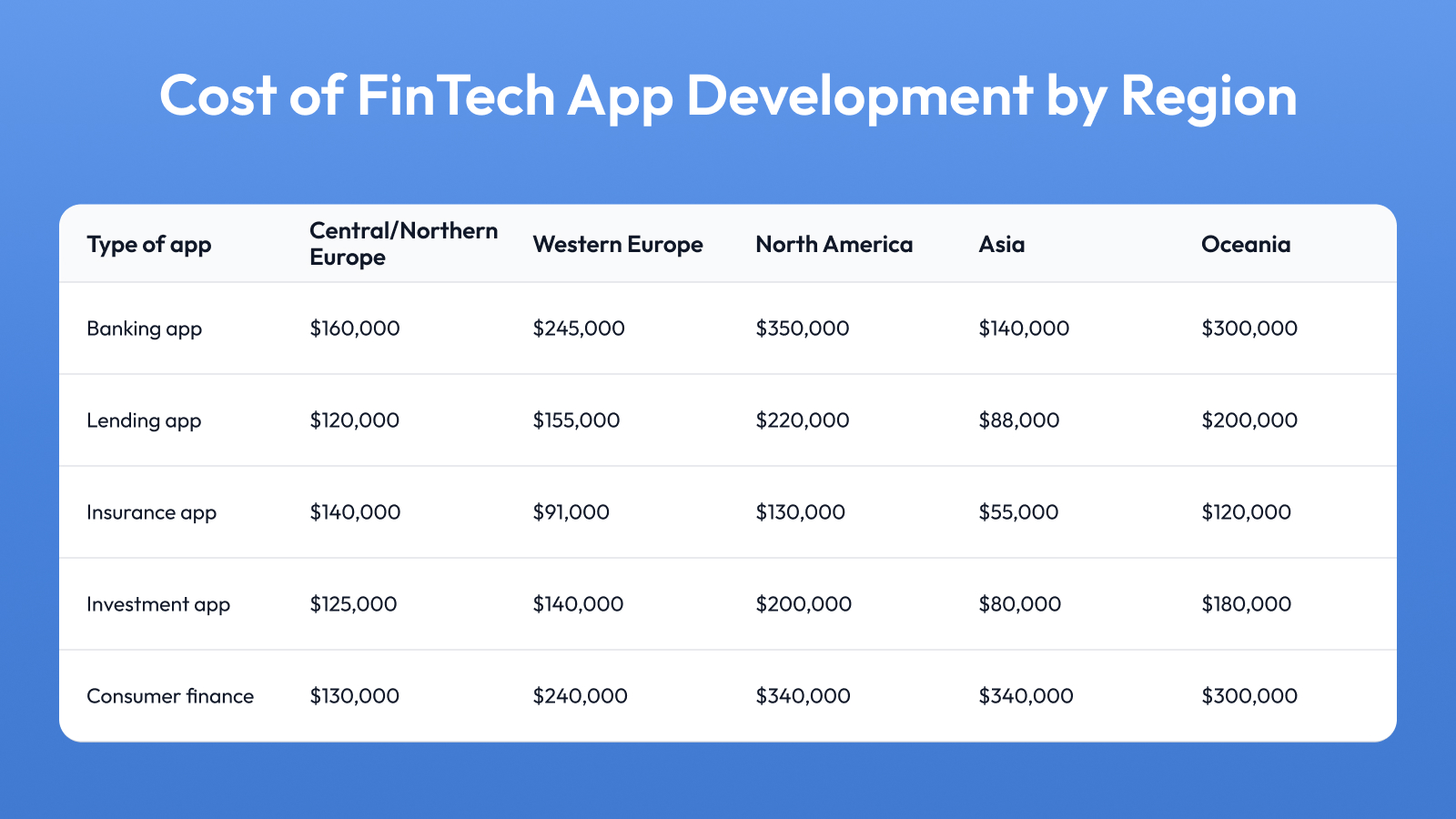

FinTech Applications Cost By Type

As we already mentioned, each type of financial application has its own features, so its price is different. Now, we will briefly overview the main FinTech app types and their costs.

Banking app

Banking applications are digital solutions aimed at expanding traditional banking institutions’ capabilities or even replacing them. Such solutions allow clients to perform various operations with their accounts via mobile devices. Banking apps usually enable you to check your balance, make P2P transactions, schedule payments, find ATMs near you, etc.

Lending app

Lending apps are created to connect people who are ready to lend money with people who need to borrow it. These platforms streamline the lending process by offering a convenient digital interface where lenders and borrowers can easily find and interact with each other. By using lending apps, borrowers can access funds quickly and often at more competitive rates than traditional financial institutions, while lenders can earn interest on their money with minimal hassle.

Insurance app

Insurance applications streamline and automate classical services. There are several types of such solutions depending on their purpose:

Claim settlement

Travel insurance

Sales management

Car insurance

Broker app

Investment app

Investment platforms are handy tools that allow beginners and experienced investors to manage their funding conveniently and “on the go.” So how to build an investment platform? Remember that it should provide rich functionality that includes not only basic features like buying and selling assets but also comprehensive analytics and reports to help users make informed and effective decisions.

Consumer finance app

This FinTech app type is aimed at effective finance management. It provides wide functionality, allowing users to control their spending by categories, set goals, and control their performance.

What’s the bottom line? The time and costs required to develop these solutions vary. Here are the approximate calculations based on the hourly rate of $50 per hour, which is typical for the Central and Eastern Europe (CEE) region.

How The Choice Of IT Partner Impacts FinTech App Development Costs

So, we’ve already explored some of the critical FinTech app’s cost-driving factors. Now, we should discuss how your software development team’s selection may affect the price:

Cooperation model

There are three possible hiring options for FinTech app development:

In-house team. You can hire a whole development team to work in your company. This option provides you with the highest control level but implies additional expenses for office rent, hardware, wages, insurance, etc.

Staff augmentation. You can hire all essential specialists from an outsourcing software vendor but still maintain complete control over your project. This option allows you to save time on hiring and cut expenses.

Dedicated development team. This cooperation model implies hiring a whole team for FinTech app creation from an outsourcing provider. You completely outsource your project to an external vendor, freeing up your time for other business tasks.

Region and hourly rate

Another factor that has a tremendous influence on the FinTech app cost is your software development team’s hourly rates. This variable depends on geographical location. The cheapest regions are Asia, India, and Latin America: they offer software development services at $40-$60 per hour. Canada, the USA, and Western Europe are the most expensive ones – IT specialists here charge $100-$200 hourly. The most popular outsourcing regions today are Central and Eastern Europe. It is famous for a huge number of software providers who provide high-quality services at a reasonable price – $50-$80 per hour.

You can see how your software provider’s location can impact the cost of building a FinTech app below:

Conclusion

To summarize, the cost of FinTech application development can vary from $50,000 to $350,000+. The exact numbers depend on a vast array of factors we’ve explored in this article. If you want to get a detailed estimate, you should turn to a reliable software provider with deep expertise in the FinTech domain and share the idea of your future project. Thus, you’ll receive not only price calculations but also comprehensive consulting and development services.

Author bio

Yuliya Melnik is a technical writer at Cleveroad, a software development company in Ukraine. She is passionate about innovative technologies that make the world a better place and loves creating content that evokes vivid emotions.

An essential security tool for contemporary digital interactions, SMS two-factor authentication (2FA) offers a much-needed layer of protection for consumers and companies.

Depending just on passwords is insufficient in a time when data breaches and cyber-attacks are rather common. Before granting access to private data or accounts, SMS-based 2FA adds a checkpoint for verification.

On their mobile device, the user gets a special, time-sensitive code that needs to be entered to finish the authentication process. This approach guarantees that a password should be hacked; illegal access is still improbable without user phone access.

Basis of SMS Two-Factor Verification

SMS two-factor authentication depends on creating a temporary code the system sends to the mobile phone of the user. This process begins a secondary step for confirmation following user password submission. Usually good for a limited period, the one-time passcode (OTP) produced by the service provider is sent to the registered phone number.

The user then codes to finish the verifying process. This guarantees that the one trying access is actually the account holder. In this process, sms verifiers are indispensable since they control the delivery of verification codes to the right user and make sure that the communication stays safe.

Two-Factor Identity Evolution

At first, security policies concentrated on password-alone use. However, the increasing complexity of cyberattacks made it abundantly evident that more powerful approaches were required. For most people, SMS verification thus became an easily available, user-friendly solution.

Although app-based verification and biometric scanning are increasingly popular as alternate forms of 2FA, SMS verification is still a favorite because of its simplicity and general availability. Many portals and systems have embraced SMS verifiers to guarantee safe access.

Improved Security Using SMS 2FA

It is impossible to overestimate how much SMS two-factor authentication strengthens online security. No matter how sophisticated, passwords are susceptible to phishing, brute force, and keylogging, among other attacks. With SMS verifiers, SMS-based 2FA creates a barrier that practically makes it impossible for hackers to obtain access without the user’s phone. This approach guarantees that unauthorized access is denied even in cases of stolen or guessed passwords, so greatly lowering the possibility of account breaches.

SMS 2FA also offers instantaneous reactions against questionable behavior. For example, the SMS code acts as a last checkpoint before access is granted if someone attempts to log in using an unknown device or location.

Typical Uses for SMS Two-Factor Authentication

Two-factor SMS authentication is used in many different sectors to protect online transactions and passwords. Financial services have especially included this approach to protect online banking and payment systems. Likewise, digital service providers and e-commerce sites depend on SMS-based verification to guard private user data, including addresses and payment details.

SMS verifiers such as Syniverse help companies simplify this process and provide their consumers with flawless security. Healthcare facilities also use SMS 2FA to control access to private patient records, guaranteeing adherence to data security rules. Moreover, it is extensively embraced in corporate settings where access to internal networks and corporate accounts has to be controlled to stop illegal access.

Alternatives to SMS 2FA and Limitations

Though SMS two-factor authentication has great security advantages, it is not without restrictions. SIM swapping—a kind of fraud whereby attackers take over the victim’s mobile number and intercept SMS codes—is one main issue. Furthermore, inadequate mobile network coverage can occasionally cause delays or prevention of verification code delivery, inconveniencing users trying to access their accounts.

Many companies are investigating alternative forms of 2FA, including app-based authentication or biometric verification, to get beyond these constraints. While providing a smoother and safer user experience, these techniques remove the dangers connected with SIM swapping and network problems. Nonetheless, for most consumers and companies, SMS 2FA combined with trustworthy SMS verifiers remains a useful and generally accepted way to provide consistent defense against illegal access.

Conclusion

SMS two-factor authentication is a must-have tool since it provides an easily available and efficient means to prevent illegal account access. SMS verifiers help companies to provide quick and consistent authentication, so guaranteeing that only authorized users can access. SMS-based 2FA remains a key component of safe authentication systems for anyone looking to improve their security without needless complications.

Since customers today have an excess number of product or service options, it follows that there is no certainty that your brand would be favored or liked over another. Therefore, startups must invest much energy into amplifying their brand value and fandom like never before.

Fortunately, a new generation of startups is reshaping the concept of brand loyalty banking on technology. Unlike giant corporations of yesterday, empowered by solid market presence and established concepts, technology isn’t just a means for these agile innovators. The foundation of their whole brand creation remains a technology-oriented venture.

Those tech-based newcomers who often ascend to the top do not do it by mere chance. They have a profound focus on philosophy and purpose. Hence, the question is, how does a startup ideally move from recognizing technology’s role in strengthening brand value to converting it into a tangible measure?

The Role Of Technology In Enhancing Brand Loyalty

Optimize user experiences

If you have ever visited a website that was so difficult to navigate that you had to opt out prematurely, then you know how crucial user experience (UX) is in the customer’s life journey. A poor UX is a big turn-off for potential clients and portends catastrophic repercussions.

The customer onboarding process must be user-friendly and intuitive. Indeed, 40% of clients said their future purchasing decisions predate their first user experience with a brand.

A well-trained customer support system is crucial to offering timely responses to customers and escalating matters that need the scrutiny of subject matter experts.

Personalizing your content to your customers’ unique needs makes them feel more understood and appreciated, which increases their affinity for your brand. In reality, 83% of customers interviewed by Shopify, said they expect more personalized and engaging content.

Technology is a powerful tool for startups that can facilitate the delivery of dynamic and personalized interactions. Data analytics is used to mine customer databases to discover patterns in their online behaviors and other engagement metrics. For example, using tools like the best CRM software for restaurants can help identify customer preferences and tailor communication accordingly, enhancing loyalty.

You can also use different automation tools and chatbots to deliver convenient, immediate responses and recommendations. According to a Harvard Business Reviews study, 81% of customers would engage a chatbot in customer service rather than wait for a human being to resolve their issues.

Leverage social media

Did you know that over 4.8 billion people are on social media? Even more astonishing is that three-quarters of the globe’s population over 13 years of age is actively engaged on social networks.

The point is that technology is a crucial enabler for amplifying brand value by allowing customers to connect, engage, and personalize their experiences.

By engaging with brands on social media, customers can develop a sense of belonging which may turn them into passionate supporters.

Conclusion

In the digital world today, pure brand loyalty has to be earned. For startups that want to improve their recognition and build a fanatical supporter base, the secret sauce lies in creating a community and maintaining customer satisfaction at top-notch levels. The above tech-powered strategies can help you build high-value brands that excite customers.

Today, artificial intelligence (AI) has taken over the business landscape. Generative AI is a group of high-performing algorithms using machine learning to learn and create content. Thousands of companies are using generative AI tools like ChatGPT to improve efficiency.

You can ask these tools to create powerful email messages, and they do. Some, like DALLE-2, also eliminate the need for hiring a photographer – they make high-quality images, and all it takes is a few clever prompts.

Here are a few great ideas to help you improve CX with AI.

10 Steps To Improve CX With AI

1. Elevate CS with chatbots

Maintaining 24/7 human support on a website or social media can be expensive. However, with AI chatbots, this level of support is possible at meager costs. You can implement a chatbot that helps answer customer questions or provides product recommendations.

2. Analyze customer needs

Another way to leverage AI in CX is through AI-generated surveys that aim to understand customer needs. You can use ChatGPT to quickly analyze customers’ product preferences and content consumption habits. This survey can help you in product development and marketing.

3. Accelerate social media results

Normally, success on social media takes long hours of work. It also takes big budgets that lock many small businesses out of success potential. With AI tools like DALL-E2, you can quickly generate eye-catching images for your content and promotions. You can automate the entire process of creating content, posting, and tracking performance.

4. Generate content at scale

Small businesses with no resources to hire or retain a marketing team can turn to generative AI for help. They can work with AI to generate massive product descriptions for e-commerce stores, social media posts, and website copy. It is possible to work with these tools to tailor the tone and style of the message to align with customer needs and expectations.

6. Multilingual customer engagement

AI can help you make your marketing accessible to people from all over the world. You can instantaneously translate company website content to serve different regions. Compared to hiring and retaining customer support teams across, the AI approach is more cost-effective.

7. Create segment-driven CX

AI is useful in analyzing and understanding different customer segments and how they interact with your products. You can then use these insights to create impactful experiences accurately tailored for each segment and their culture and preferences.

8. Identify trends and patterns

AI analytics tools like Microsoft BI can help you study large data volumes and helpful patterns. These patterns can help you predict customer behavior and create highly effective products. You can also use the insights in web design, marketing, and customer support.

9. Reduce churn rate

You can use AI tools to understand important customer behavior related to loyalty. You can then use this data to create campaigns and messaging that elevate retention.

10. Power human-centric interactions

With AI in play, it is essential to create human-centric brand experiences. Ironically, AI can help with that, too. You can use highly trained AI tools to give intuitive answers to customer questions. If these responses are made in a natural and conversational tone, it will lead to high engagement and personalized experiences.

Conclusion

AI can significantly help you improve customer experience. In the current highly competitive business environment, smooth and memorable experiences can be the difference between success and failure. Use these tips to stay ahead.

Every business is constantly looking for new ways to reach their potential customers and with more than 2 billion monthly users, Google Maps is one of the most effective platforms to do just that.

Most people rely on Google Maps via smartphones for daily decisions. Customers often search for business information, contact details, reviews or directions on Google Maps. Businesses can leverage this power to thrive in this digital landscape. Whether you have a restaurant, clinic, retail store, salon, appearing in the search results of Google Maps is a necessity for your business. That’s where Google Maps Advertising comes into play.

These hyper-targeted ad campaigns boost your business’s visibility and increase the real-world visits to your physical store.

In this article, we will walk you through everything you need to know about Google Maps Ads. Get ready to put your business on the map, literally.

What are Google Maps Ads?

Google Maps Ads are a form of location-based advertising that help your business to appear at the top of the search results, leading to increase in awareness about your physical store or service.

For instance, if someone searches for the “Best café,” your business can appear at the top of the map results with a tag like “Ad” or “Sponsored”. This will also Google Business Profile details, such as name, location, ratings, operating hours, contact details and directions.

Google Maps is the top navigation application on both Android and iOS, giving your business a major competitive edge in local search.

What are Different Types of Google Maps Ads?

Google Maps run ads in various formats including:

Sponsored Search Results: When a user searches for a specific product or service in your niche, your business appears at the top of the search results.

Promoted Pins: Eye-catching square pins with your brand logo appear when users browse the map of a specific area. Tapping the pin reveals your business details.

Promoted Pins Along a Route: When a user navigates to a destination, your business may appear along the route. An additional “Add stop” button is added to make it easier for users to visit your location.

Benefits of Google Maps Ads

With over 10 billion downloads on Android alone, the reach of Google Maps is undeniable. Here’s why your business must leverage the potential of Google Maps marketing:

Boost in Local Visibility- Your business shows up at the top of local searches, increasing the chances of grabbing the attention of people. Rather than investing hefty expenses on traditional ads, Google Ads is a cost-effective method to directly increase your business searches.

Builds Customer Trust – Only verified businesses can run Google Maps Ads since they need to go through a strict screening process. Additionally, when customers see all the accurate information at the tip of their fingers, it builds a sense of trust towards the business.

Advantage over Competitors – Many local businesses have not tapped into Maps ads yet, giving you a competitive edge as an early adopter to reach more people and turn them into loyal customers.

Increase in Store Footfall – Since Google Maps Ads are a geographically targeted search, users close to your location are more likely to visit your location when the ads are displayed to them at the right time.

Measurable ROI – Track the effectiveness of your Google Maps Ads through comprehensive analytics provided by Google, enabling data-driven decisions.

Visit https://www.algosaga.com/blog/google-maps-marketing/ to know more about Google Maps marketing solutions.

How do Google Maps Ads Work?

Google Maps Ads are location-based promotion campaigns that you run to gain maximum customer attention and here’s how they operate:

User Search: User searches for a specific product or service such as “restaurants near me” on either Google Maps or Google search with a local intent.

Ad Trigger: If you are running a Google Maps Ads campaign, your ad will get triggered based on the proximity, keyword and relevance of the user’s search.

Ad Display: Your business will appear above all organic results with a “Sponsored” or “Ad” tag.

User Action: Users can call directly, get directions, read reviews, visit your website or take other actions based on your CTA. Let’s say, the user finds a restaurant they like and proceeds with booking a table.

How to Start Advertising on Google Maps?

Setting up Google Maps Ads can seem daunting but follow this step-by-step guide to add your business to Google Maps:

Verify & Optimize your Google Business Profile

Only business profiles can use Google Maps Ads since it legitimises the business.

Open Google Business Profile and set up your listing.

Add all the latest details such as product/service descriptions, website link, contact, photos, opening hours, chat feature and more to make it stand out.

Complete the verification process with a confirmation code via phone.

Create a Google Ads Account

Open Google Ads, go to the “All campaigns” page and click on “+New campaign”.

Choose your Business profile and link your website. Click on Next.

Choose your main advertising goal and proceed ahead to complete the process.

Launch a Local Google Maps Ad Campaign

Navigate to the “Campaign” section and select “New campaign”.

Under campaign type, select “Local” and then, click on “Google Maps ads” as the campaign subtype.

Define Targeting

To narrow down your target audience, you need to specify the geographical area, keywords and queries you want to target. To improve your visibility, ensure you conduct proper keyword research to identify high search terms.

Develop your Ad

Write a compelling headline, description and clear call-to-action (CTA) for your business. Add brand visuals like logos and images to stand out.

Launch & Monitor your Campaign

Once your ad is active, you can track its performance using various metrics like clicks, impressions, click-through-rates, conversions etc. Continuously review and optimize your campaigns based on data insights.

How Do You Measure The Success of Your Google Maps Ads?

Understanding how your ads are doing is crucial to ensure your campaign is performing well and identify areas of improvement whenever required. While store visits and phone calls provide basic indicators, Google also offers in-depth metrics to track user engagement, offline visits, conversion rates and overall effectiveness. Here are some key ways to measure success of your Google Maps Ads-

Impressions: Reflect how often your ad was displayed on Google Maps. Aim for high impressions as they portray good visibility.

Click for Directions: Indicates how many users clicked to get directions to your store and offers insights into the potential footfall generated by your ad.

Website Clicks: Track how many users clicked on your website directly through Maps ads.

Click-Through Rates: A high CTR is an indicator of engaging ad copy and visuals that are resonating well with the users.

Conversion Rates: Measures the percentage of users who completed a desired call-to-action, such as making a purchase or booking a service.

User Behaviour Insights: With tools like Google Analytics, you can analyse how users interact with your website after clicking on the ad.

Final Thought: Optimize Your Google Maps Ads with an SEO Expert

Google Maps Ads are becoming one of the most powerful tools for business owners to attract new customers and increase your business visibility.

However, when they are paired with expert SEO, they deliver unmatched results. AlgoSaga SEO services specialize in delivering real-world results through data-backed strategy. Whether you are a restaurant, clinic or retail store, Google Maps Ads combined with AlgoSaga’s SEO expertise can help you to get discovered at the right time by the right audience.

The banking industry is in the midst of a digital revolution. Gone are the days of long queues and endless paperwork. Today, customers expect seamless, secure, and instant access to their financial services. Enter Artificial Intelligence (AI) and, more specifically, facial recognition technology. This powerful combination is not just a futuristic concept; it’s rapidly becoming the bedrock of enhanced user authentication in banking, offering unprecedented levels of security and convenience.

The Evolution of User Authentication in Banking

For decades, traditional authentication methods like passwords, PINs, and security questions were the standard. While they served their purpose, they were often cumbersome and vulnerable to fraud. Phishing attacks, data breaches, and the sheer human tendency to reuse simple passwords posed constant threats. The need for a more robust and user-friendly solution became glaringly apparent. This is where the transformative potential of AI in banking truly shines.

The Power of Facial Recognition in Financial Security

At its core, facial recognition technology analyzes unique facial features to verify a person’s identity. In banking, this translates to a highly secure and convenient way for customers to access their accounts, authorize transactions, and even open new accounts. But how does it work, and what makes it so effective?

Imagine a scenario where you want to log into your mobile banking app. Instead of typing in a password, you simply look at your phone’s camera. Within seconds, the AI-powered system analyzes your face, compares it to a stored template, and grants you access. This seemingly simple process involves complex algorithms and machine learning models that can detect subtle nuances in your facial structure, even distinguishing between identical twins in some advanced systems.

Key Benefits of Facial Recognition in Banking:

Enhanced Security: Facial recognition offers significantly higher security than traditional methods, making it difficult to spoof.

Improved User Experience: Provides unparalleled convenience; no more remembering complex passwords.

Fraud Prevention: AI algorithms, coupled with facial recognition, expertly detect suspicious activity.

Faster Transactions: The speed of facial recognition leads to quicker transaction processing.

Accessibility: Offers a more inclusive way for individuals with disabilities to access banking services.

The Role of Artificial Intelligence in Bolstering Facial Recognition

While facial recognition is the front-facing technology, Artificial intelligence is the invisible engine that makes it so powerful and reliable in the banking sector. AI algorithms continuously learn and adapt, making the authentication process more robust and resilient to new threats.

Here’s how AI enhances facial recognition in banking:

Machine Learning for Accuracy: AI-driven machine learning models are trained on vast datasets of facial images to improve accuracy.

Anomaly Detection: AI excels at identifying deviations from typical user behavior or facial characteristics, flagging potential fraud.

Deep Learning for Liveness Detection: Advanced AI techniques ensure the system interacts with a live person, not a static image or video.

Continuous Improvement: AI systems are designed to continuously learn and update, countering new fraud techniques as they emerge.

Real-World Applications and the Future of AI in Banking Authentication

Many leading financial institutions worldwide are already implementing or piloting facial recognition solutions as part of their AI in banking strategies. From mobile banking app logins to ATM withdrawals and even branch customer identification, the applications are vast.

Consider the example of a major bank that implemented facial recognition for mobile app logins, reporting a significant decrease in fraud and improved customer satisfaction. Another bank is leveraging facial recognition at ATMs, allowing cardless cash withdrawals and reducing skimming risks.

Looking ahead, the integration of AI and facial recognition in banking is only set to deepen. We can expect:

Multi-modal Biometrics: Combining facial recognition with other biometrics like voice or fingerprint scanning for stronger authentication.

Behavioral Biometrics: Analyzing user behavior patterns (e.g., typing speed) alongside facial recognition for comprehensive risk profiles.

Enhanced Personalization: AI can use facial recognition to personalize banking experiences, for example, by instantly identifying customers in a branch.

Regulatory Adaptation: Regulatory frameworks will continue to evolve to ensure data privacy and ethical use of facial recognition.

Addressing Concerns and Ensuring Trust

While the benefits are clear, banks must address concerns around data privacy and security when implementing facial recognition. Transparency in data handling, robust encryption, and adherence to strict privacy regulations (like GDPR) are paramount. Banks must communicate how facial data is collected, stored, and used, assuring customers that their sensitive information is protected.

Conclusion

The convergence of AI in banking and facial recognition technology is fundamentally transforming user authentication. It’s moving us towards a future where banking is not only more secure but also more convenient and intuitive for everyone. By embracing these advancements responsibly, financial institutions can build stronger relationships with their customers, enhance operational efficiency, and ultimately, secure their place in the rapidly evolving digital financial landscape. The days of struggling with forgotten passwords are fading, replaced by a glance that unlocks a world of secure and seamless banking.

Augmented Reality is transforming technical training in education and industry in real time. Be it assembling a jet engine or performing a heart surgery without touching a single tool or patient, AR is doing it all!

Sounds futuristic? Well, augmented reality is today’s reality.

Augmented reality in education and industry is quietly changing the way we teach and learn technical skills across classrooms, workshops, and factory floors, with interactive learning layered over the real world. In the AR world, mistakes do not break machines, and learning can happen anytime, anywhere.

Changing the Classroom: From Theory to Immersive Learning

In schools and colleges, AR is making technical subjects come alive. A student in a biology lab can now just point a tablet at a printed diagram and watch a beating 3D heart float above the page.

Or an engineering trainee can walk through a virtual cross-section of a turbine engine to easily understand its components with the swipe of a finger.

This shift is already underway.

Several schools have launched AR and VR labs to help students from under-resourced backgrounds explore STEM concepts in immersive detail, wherein they can see, touch, and manipulate the concepts they are learning.

For higher education, especially in technical institutes, AR allows complex, often dangerous processes to be practiced safely and repeatedly. From circuit design to welding techniques, learners can build muscle memory in virtual environments before stepping into real-world scenarios.

On the Job: How AR is Revolutionizing Industrial Training

The impact of augmented reality is even more pronounced in industries where training can be costly, hazardous, or simply hard to scale. Here are a few ways AR is revolutionizing industrial training:

In aerospace, companies like Red 6 are training fighter pilots using AR overlays. It cuts down flight hours and brings consistency to pilot readiness.

In healthcare, AR tools help trainee surgeons walk through procedures using holograms. The technology provides step-by-step guidance without needing a cadaver or expensive simulators.

In manufacturing, AR glasses assist new employees with real-time assembly instructions to improve accuracy and reduce downtime.

The result?

Faster training

Fewer errors

A more confident workforce

Why It Works: The Core Benefits

AR’s strength lies in how it engages both the visual and tactile senses. Learners get to interact with their environment, which leads to higher retention, better understanding of spatial relationships, and more effective skill-building.

It also democratizes training as it allows organizations deliver consistent, high-quality training right on the floor, or even remotely. This means that they don’t need to spend money on sending students to central hubs or setting up costly machinery.

Learners can also practice as many times as needed, confidence builds without fear of failure.

Still Early, but Promising

Of course, the road is not without hurdles. High setup costs, lack of technical know-how, and resistance to change remain real concerns, especially in institutions with limited budgets or entrenched systems.

But the tide is turning.

AR hardware is becoming more affordable. Platforms are more intuitive. And as AI and AR begin to integrate, we can expect intelligent training systems that adapt to each learner’s pace and style.

In a world where skill gaps are widening and speed matters more than ever, an augmented reality system for technical training offers something rare: depth without delay, precision without pressure. Whether in a rural classroom or a high-tech factory, it is helping us train faster and smarter.

And that may be the real revolution.

In the last few years, artificial intelligence within the FinTech domain has revolutionized the manner of conducting financial processes. Algorithms nowadays have a massive impact on improving various aspects of the financial industry, starting with enhancing customers’ experiences to fighting fraud. In this article, we explore five exciting ways AI-driven algorithms transform and improve financial activities.

Major Applications of AI in FinTech

Nearly 70% of financial institutions use AI elements (machine learning, predictive analytics, robotic process automation, etc.) to optimize internal operations and increase revenue. Let’s define other 5 key ways AI can come in handy within the FinTech industry:

1. Fraud Detection

This is due to the nature of AI capabilities where it excels at financial fraud. Knowledge and analysis of thousands of fraud scenarios reveal techniques of fraud that human beings cannot detect. For example, Visa’s AI-driven real-time fraud detection increased the fraud detection rate by 54% compared to usual banking systems. AI-powered fraud detection is online 24/7 and instantly detects fraudulent actions; this use identifies fraud based on customers’ actions and improves its predictions.

The application of AI in FinTech improves customer safety, especially in the banking sector, increasing users’ trust in the software and promoting business productivity due to strong protection.

2. Enhanced Customer Service

Traditionally, the customer interface in a financial organization was managed by officers, and the system had its weaknesses due to irritability and tiredness. AI, however, comes with a more efficient means through chatbots and robo-advisors, changing the focal point to the customer experience, while CRM in FinTech further enhances this interaction by providing personalized insights and tracking customer preferences.

Users must be informed of changes regularly, accounts handled effectively, complaints solved, information given to customers, and problems solved in the best ways possible; this is why chatbots are crucial.

Also, there are robo-advisors used for FinTech personalized virtual portfolio managers. They test levels of risk-taking, select investment plans, and make purchases or sales depending on current market trends. These digital assistants are important for financial advisory services and stock exchange operations because they provide simple yet professional tips concerning investment.

3. Risk assessment in lending

Advanced credit analysis is already changing the lending business with the help of AI. Banks and P2P lending companies apply AI to process massive amounts of data that provide detailed insights into customers’ behavior to improve lending risk assessment and automate loan origination.

In the FinTech lending area, machine learning plays a significant role as it helps to automate credit risk models and decision-making. They enhance the identification process in light of effectively authenticating an applicant’s identity and using the identification instrument to enhance secure transactions.

AI also optimizes credit administration in terms of loan documentation verification. Employing AI technologies in P2P lending enhances performance, process optimization, and customer confidence due to strong security measures. They are here on our team to optimize these platforms, especially with AI integration to increase performance and security for financial transactions.

4. Insurance Recommendations

The insurance recommendations are shifting to using larger data sets for recommendation as artificial intelligence rolls on. This approach enhances completion accuracy through demographic, risk, and coverage coverage parameters.

AI also accelerates insurance operations, transforms work tasks, and optimizes decision-making through the use of big data and analytics. This is helpful not only in increasing customer satisfaction through personalized recommendations but also in improving operational effectiveness and decreasing costs.

5. Investment Analysis

For example, hedge funds, which were available only to high-net-worth individuals for years, leverage superior artificial intelligence to transform data processing. Some have already embedded computational models for automated investing, but the results have often been poor. However, AI in FinTech can potentially upgrade many of these automation processes.

Suppose a hedge fund where stock operation occurs based on artificial intelligence; the artificial intelligence constantly analyzes the stock market trend and proceeds with necessary actions every day to achieve the necessary goals. This innovative approach simplifies investment procedures and enables investors to manage their plans for better results and boost profitability.

Difficulties and Questions of Professional Ethics

If you have ever thought about how to create a banking application, blockchain service, or more, remember that AI in the context of FinTech may provide a vast array of neoteric challenges. Ethical questions need to be addressed in order to achieve a working path that is both sound and responsible.

Data Control, Protection, and Security issues

Preserving data privacy and security is currently the biggest challenge if AI is to be implemented in the FinTech industry. Banking and financial institutions hold monumental libraries of clients’ valuable information, thus making them prime targets for cybercriminals. As is known, adopting AI enhances data analysis but brings new risks. The amount of data that is fed to learn the AI models is humongous, and this is why the confidentiality of the task is at risk.

To protect against unauthorized people accessing information, tough measures of protection regarding the conversion and storage of data and strict access rules need to be implemented. These measures are protective barriers that help prevent the violation of customers’ information.

Ethics of AI in Decision Making

In FinTech, AI algorithms have gained quite much control over important decisions that define people’s finances, from credit scores to loans. However, all these decisions continue to remain inherently biased. Because AI systems learn from past information, they are capable of recreating existing prejudice and, hence, unfairly treating certain groups.

AI models may end up reproducing discriminating instances previously used to train the system, primarily because this data was input at one instance. This requires a constant proactive approach involving fairness-promoting classifier algorithms that work proactively to counteract unfairness while making loan decisions.

Stability Aligned With Customer Expectations

Again, AI is promising for financial services, but keeping the trust is the ultimate goal. There is a positive obligation to ensure data protection and the fairness and explainability of AI-derived decisions. It thus takes financial institutions around to explain how the use of AI technologies happens and the measures being taken to ensure that customers are protected. Letting the customers know how the AI operations work and providing them the ability to dispute/understand these operations are the fundamentals on which this trust is built.

Accountability and Transparency

The general process of decision-making is not easily comprehensible with less transparent AI models, such as elaborate machine learning models, bringing about the “black box effect”. This lack of transparency presents accountability issues. A key next step in AI risk management is the effort made to improve the transparency and interpretability of AI decision-making. They also can provide interpretations on how a particular model reaches one result or another, which explains increased accountability and trust.

Future Trends and Predictions of AI in Fintech

Thus, the advancement of AI in the world of FinTech illustrates the continuous development paradigm that will offer tremendous growth in the future. Exploring this complex cross-section uncovers important evolutions and prognoses that promise to reshape the FinTech space.

Enhanced Personalization

In particular, in the sphere of AI-utilizing FinTech, one of the significant trends of the upcoming years is vast personalization. In the future, financial services will deliver personalized services because AI algorithms will improve with technological advancement. It is expected to usher in tailored financial planning, advisory services, unique investment solutions, and tailored banking, all of which will skyrocket customer satisfaction and loyalty levels.

Convergence with Blockchain

It has been noticed that the integration of AI and blockchain technology is going to bring revolutionary changes to the field of financial technology. I have determined that AI’s integration can improve consensus algorithms, resource management, and predictive modeling for blockchains. This synergy is intended to help improve security and governance within various financial systems involved in adopting and applying blockchain technology through the several applications of using smart contracts and decentralized finance (DeFi) among others.

Ethical AI and Regulatory Frameworks

As the use of AI continues to grow in the FinTech space, so too will concerns about ethics and regulations. Future regulations are more likely to attach heavyweight to fair, transparent, and accountable uses of AI-related technologies. Lenders should incorporate ethical standards of artificial intelligence to curb biases and discriminate against AI algorithms. Supervisory authorities will become key stakeholders in the development of more rules and regulations concerning the use of AI systems in the context of the financial industry.

Let’s Sum Up

Artificial intelligence in FinTech is indeed bringing a revolution in the financial industry. There is anticipation of such services as customized services, strong protection against fraudulence, artificial intelligence planning, blockchain integration, and self-executing finances.

As a result, managing the future requires ethical standards of AI and regulation by financial firms. The potential? Innovation on a grand scale, bigger productivity, and increased satisfaction of clients. Responsible AI deployment makes financial institutions adopt leading solutions to serve customer needs.

Author bio

Yuliya Melnik is a technical writer at Cleveroad, an inventory management software development company in Ukraine. She is passionate about innovative technologies that make the world a better place and loves creating content that evokes vivid emotions.

The cryptocurrency industry has transformed itself to be a niche but one of the most groundbreaking financial systems of the current age. Nevertheless, as it has grown fast, the concerns regarding fraud, scam, and identity theft have been questioned more than ever. Since the mainstream adoption of digital currencies, user trust has never been as significant as it currently is. This is where Digital ID Verification of Crypto is involved.

Crypto Identity Verification makes platforms not only defend themselves but defend their users and the integrity of the whole digital financial network. Through enforcing the authenticity of every transaction, the id verification systems are transforming the crypto space to be a safer, more transparent, and trusting space to everybody involved.

The history of Trust in cryptocurrency

The idea of anonymity was one of the largest attractions of crypto in early Bitcoin. Users were able to exchange and transfer assets without disclosing their personal information. However, this freedom was also the reason why bad actors utilized crypto to do illegal or unethical acts. This over time posed a great challenge to the legitimacy of the industry.

Identity Verification of Cryptocurrencies was required in order to address this problem. Exchanges and wallets began to have strict verification criteria, meaning that users had to verify themselves before they could trade. This action was a significant shift in the crypto sphere. What was perceived as a decentralized wild west started taking a new shape to become a controlled and safer form of investment to both institutional and investors.

The move to Digital Identity Verification of Crypto is not only about compliance requirements, but also about regaining trust. Users have more confidence to invest, trade and participate in the market, when they understand that a platform has a high regard to security and transparency.

The Digital ID Verification of the Crypto Industry

Id verification is a technological, data, and security process in crypto platforms. It begins when an individual creates an account of a crypto exchange or wallet. They are required to provide them with identification documents which could be a government issued ID, passport or a driver license. The system then does a check of identity verification to ensure that the information given is genuine.

The new identity authentication methods employ technologies such as artificial intelligence, machine learning, and biometrics to determine if the user matches the image on the presented ID. There are systems that even apply the liveness detection system, which checks whether the verification is made by a real person or a photograph or a video replay.

Interestingly, these systems share similarities with secure call management platforms that rely on AI and verification technologies to confirm caller identity before sharing sensitive financial or account details. This connection shows how digital ID verification extends beyond crypto — it’s shaping the future of trust across all digital communication channels.).

The importance of Crypto Identity Verification

The Crypto Identity Verification is much more than compliance. It concerns the creation of a trucking atmosphere in which trust in the giving is a must. With hacking, rug pulls, and scams being a common occurrence in a market, creating accountability by confirming the identity of each user account provides an extra benefit of accountability that benefits both the service provider and the user.

With id checking, the criminal can hardly create a fake profile or partake in criminal activities on platforms. Each authenticated account is associated with a real individual that discourages bad actors and makes the trading environment transparent. Additionally, identity authentication systems would help to trace suspicious activities since the regulators can easily fight financial crimes.

As an investor, it is a relief to know that an exchange or wallet provider performs a strong identity check verification before authorizing the transaction. It is an indication that the platform is responsible and has the interest of user safety, which is a critical consideration to new users who might still distrust digital currencies.

Improving the User Experience and Security

Among the most prominent effects of Crypto Digital Identity Verification is that it improves the user experience, as well as the security, at the same time. In the past, the user would be forced to undergo manual verification processes which were time consuming and uncomfortable. Verification is almost flawless now, as automated systems based on AI are in use.

Current verification tools consider thousands of data points in real time and identify inconsistency in a few seconds. As an example, they are able to discover counterfeited documents immediately or notice whether the face of a user does not correspond to the ID picture. Such advanced identity verification protocols ensure that the real users are on board within a short period and the fraudsters are filtered on board within a minute.

This convenience and protection balance is essential to the modern crypto business. An easy onboarding process will appeal to more users and robust identity authentication policies will guarantee continued trust and compliance. Consequently, exchanges and wallets that invest in the systems have higher chances of creating long term loyalty among its users.

The Bigger Picture of the Crypto Ecosystem

The introduction of Crypto Identity Verification systems has changed the manner in which the industry operates. It has also introduced credibility to an industry that has been accused of being unregulated. Through imposing id-checks, exchanges and DeFi (Decentralized Finance) platforms can be able to prove accountability and transparency to governments, investors and users. Moreover, with crypto still overlapping the traditional finance, powerful identity authentication mechanisms can assist in closing the gap between the two worlds. Previously institutional investors, who were reluctant to invest in the crypto world because of security reasons, feel comfortable now investing in the sphere because of the guarantee given by verified identities of users.

This change is not merely a compliance issue, but it is also a matter of redefining trust in the digital era. Digital Identity Verification of Crypto will ensure users manage their data safely, and the platforms maintain integrity without violating privacy.

The Future of Identity Checking of Cryptocurrencies

In the future, identity verification of Cryptocurrencies is more closely linked to the emergence of decentralized and self-sovereign identity systems. Such systems enable users to manage their own digital identities meaning when to share and how to share their information. This is the following step of trust in crypto whereby privacy and verification are capable of coexisting.

Identity storage based on blockchains and zero-knowledge proofs are new technologies that will additionally become safer and privacy-oriented in regard to id verification. The practices will enable the users to be able to prove their identity without giving unneeded information about personal information, hence anonymity and authenticity.

With the advancement in innovation, identity authentication will be more speedy, precise, and decentralized. Crypto Identity Verification will become even more durable because of the combination of the blockchain technology and AI, which will contribute to the evolution of the industry in a responsible and sustainable manner.

Conclusion

The cryptocurrency industry is a place of innovation, however, without trust, the innovation is irrelevant. Crypto has been verified with Digital ID which has become the basis of that trust and guarantees transparency, users protection and avoidance of financial crimes. Exchanges are not only adhering to regulations by using Crypto Identity Verification and promoting new levels of safety and wholeness with the help of the advanced identity authentication system.

In an online world where anonymity prevailed, the id verification has become the token of legitimacy. Each verified identity is one step towards a safe and globally-trusted financial system of the crypto world.